![[TSPStrategy] Getting ready for tax season - Some tax tips to consider as you plan for life after your federal career.](http://2.bp.blogspot.com/-erTXCq61ULM/TmHYAQBZ0GI/AAAAAAAACCs/6cBX54Dn6Gs/s110-c/default.png "[TSPStrategy] Getting ready for tax season - Some tax tips to consider as you plan for life after your federal career.")

Let's face it. When the topic of income taxes comes up, there are few who get excited and many who want to turn the other way. But the fact is, income tax planning is essential when preparing for retirement. If you break it up into individual parts, it's a manageable task.

Here are some tax tips to consider as you plan for life after your federal career:

1. Know your federal and (if applicable) state income tax brackets. This is necessary so you can project your cash flow in retirement to meet your living expenses. Also, you should make sure your tax withholding is appropriate.

2. Plan carefully before withdrawing funds from your Thrift Savings Plan account. Should you take funds from the TSP to pay off a mortgage, or put a downpayment on a home? Most likely, the answer will be no, because withdrawals from the TSP are fully taxable (except if you are taking qualified Roth distributions).

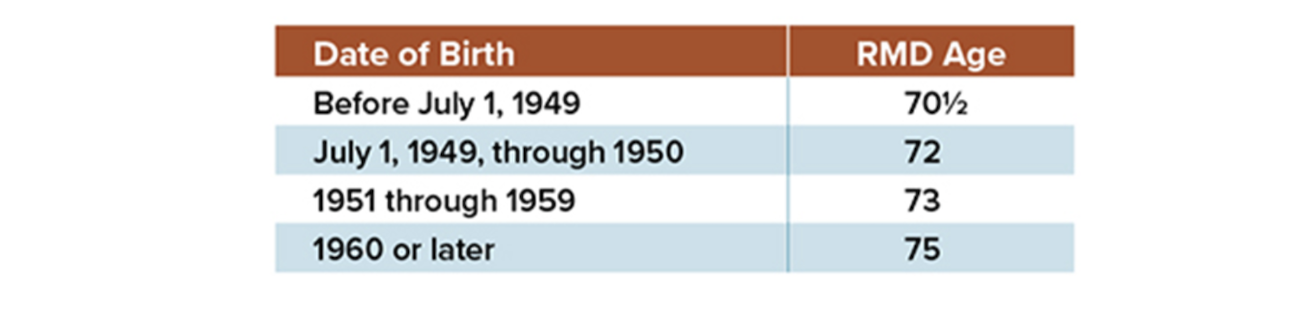

3. Remember that Social Security benefits are very income tax efficient. At the federal level, you won't pay tax on more than 85% of your benefits. There are only 11 states that tax Social Security and they are Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, Rhode Island, Utah and Vermont. You may want to consider waiting until your full retirement age (67 if you were born in 1960 or later) to apply for Social Security, because the benefit will be 30% greater than it is at 62 due to the age reduction.

4. If you are planning to retire early in the calendar year, think about "front loading" your TSP contributions. That means contributing up to the maximum elective deferral limit ($23,000 in 2024, plus $7,500 in catch-up contributions for those turning 50 or older) early in the year, since you won't be able to contribute after retirement. If you're going to start a new nonfederal job that also offers a retirement savings plan with matching employer contributions, then you may not want to do this so you can contribute to the new plan. If you're under the FERS, as most current federal employees are, keep in mind your agency's matching contributions are on the first 5% of your biweekly allotment. Decide on a contribution amount you are comfortable with since your increased contribution will affect your cash flow. If you choose to front-load your TSP contributions, look at your income tax withholding. It may be possible to decrease your withholding since the portion of your salary being invested in the TSP will not be subject to tax. Here's a quick calculator: How Much Can I Contribute?

5. If you are considering moving to another state in retirement, study up on how that state treats retirement income. Some don't tax annuities; some leave Social Security benefits alone and a few don't touch TSP withdrawals. Here's a list of state tax rules.

6. Initial federal annuity payments are subject to income tax at the federal level and in most states. Be aware that federal tax can be withheld from the initial annuity payments during the adjudication period -- the time during which your retirement is being processed. State income tax, however, is not withheld during this period. Once you set up OPM Services Online, you may elect to change your federal and begin state tax withholding.

7. Be aware that employees and former employees can transfer certain funds to the TSP. The TSP will accept both direct and indirect rollovers of tax-deferred money from traditional IRAs, SIMPLE IRAs, and eligible employer plans such as a 401(k) or 403(b) to the traditional balance of your account. Additionally, they will accept direct rollovers of qualified and non-qualified Roth distributions from Roth 401(k)s, Roth 403(b)s, and Roth 457(b)s to the Roth balance of your account. If you don't already have a Roth balance in your existing TSP account, the rollover will create one.

8. Remember that part of your federal annuity (FERS and CSRS) is non-taxable. The Office of Personnel Management generally calculates the nontaxable portion on Form CSA 1099R that you receive at the end of each tax year. Under some federal retirement systems, however, this calculation doesn't occur automatically. For a full discussion of federal annuity tax issues, see Internal Revenue Service Publication 721. If you are a retired public safety officer (law enforcement officer, firefighter, chaplain, or member of a rescue squad or ambulance crew), did you know that you can exclude from income the lesser of the amount of your insurance premiums or $3,000? See page 18 of IRS Publication 721 for the details.

9. From a tax perspective, the best date to retire is the one that maximizes your federal benefits and your personal finances, while minimizing your income tax. Many tax advisors really like mid-year retirement dates, assuming your main goal is not the maximum lump-sum annual leave payout at the end of the year. At midyear, you will have six more months on the job with a higher salary than the annuity (in most cases), possibly a bigger high-three average salary and at least a small chance of a better tax deduction on your annuity. But the nicest advantage is front-loading TSP contributions.

10. If you want to move your retirement funds from one type of plan to another, the IRS allows you to do this. For example, you can convert funds from your TSP account or traditional IRA account to a Roth account. Be aware, however, that while converting your funds may reduce future tax liabilities; in the year of the conversion, you'll pay taxes on any pre-tax funds you convert.

11. Are you making contributions to a Health Savings Account? Did you know that you can withdraw money tax-free from your HSA to pay Medicare Part B and D premiums after you turn 65? The IRS doesn't, however, allow tax-free HSA withdrawals for FEHB premiums. Remember that you can't make new contributions to an HSA after you enroll in Medicare, but you can make tax-free withdrawals for other eligible medical expenses at any age. One more thing, you can't take a tax deduction and tax-free HSA withdrawals for the same expenses.

Groups.io Links:

You receive all messages sent to this group.

View/Reply Online (#3754) | Reply To Group | Reply To Sender | Mute This Topic | New Topic

Your Subscription | Contact Group Owner | Unsubscribe [prefander.leadersworkshop@blogger.com]